What is obviously true is that Spain is in trouble, and needs help. Five years after the Global Financial Crisis broke out unemployment is at 25% of the labour force (and rising), house prices continue to fall, non performing loans continue to rise in the banking sector, bank credit to the private sector is falling, and, as Finance Minister Cristobal Montoro said two weeks ago, the sovereign is having increasing difficult financing itself. Hence the bank bailout. On top of which Spain's economy is once more in recession, a recession which will last at least to the middle of 2013, even on the most optimistic forecasts, and is in danger of falling into the dynamic which has so clearly gripped Greece, whereby one austerity measure is piled onto another in such a way that the economy falls onto an unstable downward path, as austerity feeds yet more austerity. Spains citizens are naturally nervous, anxious and increasingly afraid. Hardly a dynamic which is likely to generate the kind of confidence which is needed for recovery to take root.

The economy is steadily seizing up as the release of pressure (which was previously facilitated through the devaluation mechanism) which it badly needs cannot take place. All the dials move to red, but there is no safety valve available to drain off steam, so the danger of the boiler exploding through the giving way of one joint or another grows with each passing day.

No Mea Culpa From The ECB

Advocates of the proposed Euro Area debt redemption fund - which would pool all government debt over the 60% of GDP permitted under Maastricht - do so using the argument that we should treat the first ten years of the common currency's existence as a "learning experience". Fine, but what exactly have we learnt? Surely almost everyone who has read at least one article on the Spanish crisis now knows that the issue in Spain is private not public debt. But just how did countries like Spain and Ireland accumulate all this debt? Well one thing should be clear by now, part of the responsibility for the situation lies with the ECB who applied (as they had to) a single size monetary policy even though this was clearly going to blow bubbles in the structurally higher inflation economies. And so it was, Spain had negative interest rates applied all through the critical years, and now we have the mess we have.

Back in 2006 inspectors at the Bank of Spain sent a letter to Economy Minister Pedro Solbes complaining of the relaxed attitude of the then governor, Jaime Caruana (the man who is now at the BIS, working on the Basle III rules) in the face of what they were absolutely convinced was a massive property bubble. Their warning was ignored. What could have been done, many say. Well, at least two very simple things could have been done, and well before things got out of hand - on the one hand apply much stricter loan to value and income documentation rules which offering a much higher proportion of fixed interest rate loans (quotas could have been applied), and on the other insist the Spanish government run a much higher level of fiscal surplus to drain demand from the overheating economy. Of course, the politicians were not interested in hearing about any of this, since as measures they would have been highly unpopular, but where were M Trichet and his colleagues? They were too busy presenting Euro Area aggregate data to be willing to warn about growing imbalances between the individual economies. Now of course, the imbalances are undeniable, and the ECB is having to implement an asymmetric set of collateral rules (among other things) to try to counteract their impact.

The Root Of Spain's Problem Was The Property Bubble, But The Key To The Solution Is Restoring Competitiveness

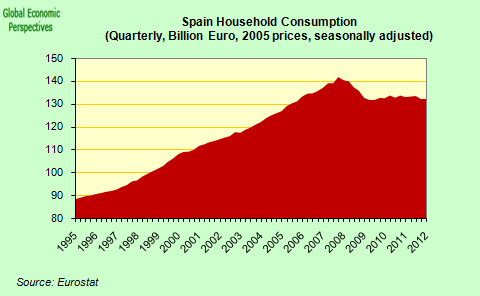

Internal demand in Spain is imploding. This is not surprising, with household debt just under 90% of GDP and private corporate around 120%, it is clear that both sectors badly need to deleverage. Classically the way to do this is by devaluing and boosting exports to sustain growth. But Spain is in the Euro, and has no money of its own to devalue. The common currency makes it very easy to generate distortions, and much harder to correct them. In that sense it is systemically biased towards negative outcomes, something the founders of monetary union didn't give enough thought to. The key institutional stabilisers - a common banking system, a common treasury, and a central bank capable of targeting interest rates on all the participating sovereigns - weren't in place from the start, and even now are considered controversial, so the constituent economies have a lopsided tendency to veer either one way or the other.

Spain's export companies have put in a heroic effort since the crisis began, and export levels have well surpassed their pre crisis peak. The problem is simply that, after years of neglect, the sector is now just too small to do the job which is being asked of it. Exports surge, even while the economy does not.

A very different state of affairs from that seen in Germany, where a revival in exports leads to strong growth. Advocates of the "competitiveness" of Spain's economy should ask themselves "why the difference?".

Another interesting comparison comes from a nice measure of capital goods investment - spending on machinery and equipment. In the German case such spending recovered sharply after the crisis, even if it has recently tailed off again as the global economy has steadily slowed.

In the Spanish case however, the recovery was muted, soon ground to a halt, and then tapered off again. That's what competitiveness means, ability to sell in sufficient quantities in global markets. Germany has it, Spain doesn't, and all the rest is simple pedantic casuistry. Or ask yourself, why is Germany bailing out Spain, and not vice-verse? Come on!

Half Finished Business

In fact, Spain has clearly carried out part of the needed correction. The current account deficit is less than half of what it was.

And the trade deficit has been reduced.

But all of this is relative. There is still a long way to go. If we look at industrial output, we will see that far from having revived it is way below the pre-crisis level, and is now falling back again.

And its the same picture wherever you look. Unemployment keeps rising.

And in recent months, as the country falls back in recession, it has been doing so at an accelerating rate.

House prices keep falling, and again at an accelerating rate. According to real estate valuers TINSA they have now fallen something like 30% from peak, and credit rating agency S&Ps estimate they have another 25% to fall, although the truth of the matter is no one really knows, since stopping the housing slide involves fixing the economy, and fixing the economy involves stopping the housing slide. Such is the double bind which Spain economic policy finds itself in. And the problem posed by falling house prices is an important one since, as we will see, the whole effectiveness of the bank recapitalisation process involves putting a floor under house prices.

Meanwhile there is little sign of credit moving in the economy, and mortgage lending outstanding is dropping by something like 2% a year.

With the evident result that there is little sign of house sales improving, despite the fact that there is now a backlog of something like 2 million unsold homes either finished or in the process of being built.

Naturally in this environment it is not difficult to understand that people are having difficulty paying their bills. Bad debts held by Spanish banks rose to yet another 17-year high in March. According to data from the bank of Spain, 8.37% of the loans held by banks, or EUR147.97 billion, were more than three months overdue for repayment in March, up from 8.3% in February--the highest ratio since September 1994. The total number of non-performing loans is now almost 10 times higher than the level reported in 2007, when Spain's decade-high property boom peaked. And of course, this steady increase will continue for as long as the economy is not fixed.

And to cap it all, the uncertainty over the future of countries like Greece and Spain is now bringing the whole global economy steadily to a halt, and this is boomeranging back on Spain, since it hits exports directly. In fact, Spain's exports have been down on an annual basis since February.

What's In A Name?

Whatever name you give to the EU financial support for Spain, one thing is clear. Spain alone was unable to go to the financial markets and raise the 100 billion Euros or so it needs to meet the capital requirements of its banking system for 2012/2013. The country’s leaders wanted one of the European funds (the EFSF perhaps) to inject the money directly into the banking system, but Europe’s leaders said no, it would need to be the Spanish sovereign that borrowed (via its bank reorganization fund FROB), and responsibility for repayment would lie with the Spanish state.

So, five years after one of the largest property bubbles in history burst, with an economy which has fallen by around 5% from its pre crisis peak and is now expected to contract by around another 2% this year, while unemployment is hitting the 25% mark, Spain has finally had to accept that it cannot manage alone.

Whatever way you call the aid Spain is now receiving from Europe it is clear that this is the beginning and not the end of what is likely to be a long process, one which will now inexorably lead to either the creation of a United States of the Euro Area, or to failure and disintegration of the Euro. There will be no middle path, so the stakes are now very high for all involved.

Unfortunately Europe's leaders are still too busy thinking short term, and practicing one step at a time-ism. In a pattern that has now become so familiar since the crisis started back at the end of 2009 with the Greek deficit problems, they are so concerned about negotiating the details of how to handle the next stage that they tend to miss the bigger picture. Essentially there are three key players in the present situation - the EU in Brussels, the German government in Berlin, and the Spanish administration in Madrid.

All three have probably walked away feeling satisfied they have gotten something out of this latest deal. The EU leadership in Brussels have long wanted to draw Spain in. After months of issues about number quality relating to both public finance and the financial system, they will now feel they have a firmer grip on the situation. They will also be perfectly well aware that Spain's financing needs go well beyond the 100 billion euros which has been agreed to as the current ceiling.

At the time of writing it still isn't clear just how much of this will be injected initially. Press leaks suggest that the figure could be between 60 and 70 billion Euros, slightly more than the 40 billion euro number recently given by the IMF. This is more or less in line with a recent report from Standard and Poor's, which said they anticipated losses in the Spanish banking system before the end of 2013 of between 80 and 112 billion Euros. Naturally recognising these losses up front now will present Spain's banking system with a difficult challenge. As Standard and Poor's say:

"In the event that banks are required to recognize provisions for 2012 and 2013 already this year, the amount of capital support that the banks could require could be substantial. This is because banks would face greater difficulty to absorb the impact of required provisions in such a short period of time with anything other than excess capital over the regulatory minimum. In this scenario, and assuming no changes to minimum regulatory capital requirements of 8% or 10% of core capital plus the buffer established by the Royal Decree 2/2012, we would expect that only Banco Santander, Banco Bilbao Vizcaya Argentaria, and CaixaBank would have capital levels comfortably above the regulatory minimum. The remaining banks in the system would likely face significant challenges to remain compliant with the abovementioned minimum regulatory capital requirements, in our view "Three points need to be made here. The first is that what we are talking about is provisioning against anticipated losses and writing down problematic assets over the two year 2012/13 period - if the economy doesn't recover and house prices continue to fall (both highly probable given the policy mix currently on the table) then further injections will be required over the 2014/15 period - although this is very academic, since the future of the Euro will more than likely have been decided one way or another by that point.

Secondly, there is the issue of how those banks who don't apply for government funds will do the necessary provisioning. Apart from operating profits, the only real measure on the table is what is colloquially know as a "bail in", whereby owners of hybrid instruments like preference shares and subordinated bonds are forcibly converted into equity. Now Spain is already reeling under the scandal of what many consider to have been regulatory negligence as the insolvent bank Bankia was allowed to go to Initial Public Offering on the Spanish stock exchange. As the Victor Mallet writing in the Financial Times put it:

The Bankia saga has prompted thousands of angry savers to consult lawyers and pressure groups, and is expected to lead to a flood of lawsuits that will cause new headaches for the government, as well as for banks and regulators already struggling to deal with the eurozone’s sovereign debt crisis. This and other cases involving billions of euros worth of products sold by Spanish banks to their retail clients will complicate any effort by bank managements or European regulators to impose losses on shareholders and bondholders to reduce the bill paid by Spanish and other European taxpayers for bank bailouts.

The debacle at Bankia, however, is merely the latest and most grievous blow inflicted by banks and cajas on Spaniards who were sold or mis-sold lossmaking financial products by their local branches.

In March, a court in Alicante ruled that Santander should return money to a client who invested in its so-called valores bonds, of which it issued €7bn in 2007 to finance the purchase of its share of ABN Amro. The Santander bonds are typical of the controversial convertible products sold by many Spanish banks, except that they are due to convert into equity at a fixed price of over €13 per share in October – and because Santander shares are now worth just over a third of that, the 139,000 retail clients who bought them stand to lose most of their capital.While details of the bank rescue package and its impact on bondholders have yet to be worked out, most analysts are busy speculating that subordinated debt holders will be forced to contribute to the recapitalisation effort. But as I say any such "bail in" would involve subordinated debt holders - and in particular holders of hybrid instruments like preference shares - taking losses. The hierarchy is just like that, you can't haircut seniors before you have hit "juniors".

These are the banks own customers, who were basically sold the instruments on the understanding that they were "just like deposits" and very low risk. Bank of Spain inspectors warned Minister Pedro Solbes in a letter in 2006 that these very instruments were being sold to finance high risk developer loans, but no action was taken. Far from making irresponsible investors pay this measure would penalise the very people who help keep Spain's banking system together, those small savers who forwent going for holidays on credit to Cancun,Thailand or Japan, and failed to increase their mortgages in order to buy lavish SUVs in an attempt to save for their retirement. These are the people who now face the prospect of losing their precious savings to cover the losses generated by those who did both of the above.

Hence the sort of bank "bail-in" EU regulators want, is politically impossible in Spain, especially after the Bankia scandal, and Mariano Rajoy knows this only too well. Only the Swedish path of direct nationalisation and subsequent resale is open to Spain. Unless, of course, your objective is to totally politically destabilise the country. As is evident, Spain's developers who offered no guarantee for their lending beyond the property are now handing back the keys and assets as fast as they can, while individual mortgage holders who guaranteed the mortgage with their lifetime salary struggle to pay down mortgages which are often now worth twice the market value of the property they are associated with. If this manifest injustice is also followed up with a wipe out of small savers while large institutional bondholders walk away scot free, well I think the next best thing to a populist revolution is what you are likely to see.

It is still unclear what conditions will be attached to the loans to cover capital needs which total around 60-70 billion euros, according to a source close to an audit of Spanish banks due to be completed on Monday. Forcing losses on junior bondholders is currently illegal in Spain, but legislation could be rushed through in an emergency situation, as it was in Ireland, lawyers and economists say. However unlike Ireland, where junior bondholders suffered losses of up to 90 percent at Allied Irish Banks and Bank of Ireland during state bail-out processes, a large part of Spanish banks' subordinated debt was sold to bank customers as savings products. Barclays estimates 62 percent of subordinated bank debt is held by retail investors in Spain, stripping out Santander and BBVA, compared to 34 percent in Ireland. Sonya Dowsett and Helene Durand writing for ReutersNaturally, the details of the loan conditions are still being negotiated, and will be become clearer as time passes. At this point I would simply emphasise three things. Firstly the money the country has asked for is not a problem fixer. It is a stopgap to enable Spain's banks to maintain capital levels as losses are crystalised over the next two years. In this sense the money addresses one of the symptoms of the problem, but not the root of the problem itself. What we can now certainly say is that Spain's banks will be well capitalised through to the end of 2013.

But credit isn't flowing to the private sector in Spain, and these funds will do little to change that situation. So this is the second point I would make, to get credit moving again a necessary (but not sufficient) condition will be deleveraging the banks - which have a loan to deposit ratio of something over 175% at present - and achieving this deleveraging most certainly means taking some of the problematic property assets off the balance sheets, to be "ring fenced" and deposited in a Nama style bad bank, for example, following the line of the reports the Spanish economy Ministry were recently reported to be studying. Doing this will need finance even after these troubled assets have been written down - it is hard to put a number till we know the extent of the write down, but 200 billion Euros would be a conservative estimate, so furbishing that finance may well be the next stage in the bailout.

Then, thirdly, we have the sovereign funding issues. As is well known foreign investors have been exiting their Spanish debt holdings, and there is no reason to imagine this posture will change. Spain's banks have been filling the gap by using LTRO liquidity to buy government debt, but there has to be a limit to this process, otherwise the banks will be as bust with the bonds as they are with the property. In fact Spain's bank dependency on the ECB is growing with every passing month, and hit 288 billion Euros in May.

But the inescapable error is in failing to inject the money directly into the banks as equity, routing the money instead through the Spanish government. By doing so, the European authorities are intensifying the “doom loop”, as one analyst puts it.So financing Spain's bond redemption needs between now and the end of 2015 – something like 200 billion Euros - plus the deficit (another 100 billion Euros, at least) will be the third bailout stage. Royal Bank of Scotland analysts headed by Alberto Gallo put the full ESM package size needed to get Spain through to the end of 2015 at between €370billion and 455billion. This seems a perfectly reasonable estimate to me. As I said, removing property related assets from the balance sheets is a necessary but not a sufficient condition for getting credit flowing. The other condition is having solvent demand, which means getting the economy moving again, and this means addressing the competitiveness issue. If the economy isn't turned round then property prices will continue to fall, and the banks will continue to have losses, which means at the start of 2014 we will need another round of capitalization just to cover for the losses to be anticipated in 2014/2015, and so on.

That link was already redoubled when the European Central Bank’s December and February longer-term refinancing operation led to Spanish banks, far more than most, recycling the cash into sovereign bonds – buying €83bn since December. Spanish banks account for a more than a third of Spanish sovereign bond ownership, nearly double the tally five years ago.

The increase has helped offset international investors’ dimming faith in Madrid – making Spain’s banks a valuable stabilising force in the country’s economy. Without them, Madrid would have little hope of financing itself. But it is a delicate and dangerous balancing act, for the banks and the country. And this bailout could be the tipping point. As well as cementing the government’s vulnerability to the banks as it transmits the bailout money to the weakest operators in the sector, there could be yet another layering of sovereign investment going the other way.

Patrick Jenkins, writing in the Financial Times

Approaching The Psychological 100% Debt To GDP Threshold

As I have been saying, Spain's debt problem was primarily one of private debt. In 2007, when the crisis started, Spanish sovereign debt was a mere 36% of GDP. This year, once the 100 Billion Euro loan for the banking system has been accounted for it will probably be very near to 90%. At the very latest it will pass through the 100% level in 2014 (that is to say, assuming there are no more "unexpected losses" to be added in the meantime - for a full account of the background to all this, see my Homeric Similes and Spanish Debt post). And it won't stop there. As long as the economy isn't fixed and returned to growth the level of public indebtedness will continue to grow, as private debt steadily gets written down and shuffled across to the public account. If the country moves to budget deficit zero, then if the competitiveness problem remains the economy will simply contract, and probably contract and deflate, which will mean the ratio will rise even without more deficits, as we are seeing right now in Italy.

But we are getting ahead of ourselves here since we still don't know how Spain and the Euro are going to get through to the end of 2012, let alone where we will be in 2014. Obviously accepting that Spain needs a full bailout is going to be hard for the German leadership, but the alternative of Spain Euro exit and default will probably prove even less appetising for them. After several years of neglect and refusing to face up to issues, talk is in the air of internal devaluation to address the loss of competitiveness Spain suffered during the boom, but so far nothing has been done. Maybe this is the next reform Brussels should be discussing with Madrid, the most recent IMF proposals certainly point in this direction . Beyond all the talking, if Europe's leaders really do want to save the Euro, and not have Spain go back to the Peseta to devalue, then one day or another this internal devaluation will have to happen or the Spanish economy will simply never recover. If it doesn’t recover then the issue will not be simply saving Spain but rather how to save the global economy when the Euro then finally falls apart. Time is now running out, as Christine Lagarde recently reminded us. I think she and Soros are being a little unfair - they have till Christmas.

This post first appeared on my Roubini Global Economonitor Blog "Don't Shoot The Messenger".

No comments:

Post a Comment